For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

The conflict across the Middle East is escalating. This is evident through the increasing number of countries becoming involved and the increasing frequency of attacks. Moreover, there is growing evidence of direct action by the key actors, such as the US and Iran, rather than just proxies.

Israel has a tendency to go hard and go early, before diplomats in the West have a chance to get organised and put together a response. This happened this time, in response to the October attacks by Hamas. However, what has surprised many, including us, is how hard the Israelis have continued to go.

It might well be that other countries such as the US and Iran don’t want a regional war, as they both state, but their wiggle room has been reduced as the conflict has escalated. Indeed, while there is little evidence of any reversal as such, there are still signs of restraint, or at least targeted escalation. For example, the assassination of military or political leaders. Hezbollah, meanwhile, is showing political and military solidarity with Hamas but is limiting attacks to the border.

However, this restraint is coming under increasing pressure as forces like Hezbollah, Iran and the US have to retain some degree of credibility in the region, even if their preference is not for all-out war. For example, the recent terrorist attack in Iran was the worst attack inside Iran since the 1979 Islamic Revolution. Iran had little choice but to respond in some way, if they want to maintain credibility.

From a number of different perspectives, it is clear the conflict is escalating. However, that’s not evident by looking at financial markets, or for that matter some newspaper headlines. The oil price, for example, looks relatively unresponsive over that period, although gold, to be fair, has rallied since the beginning of October, though part of this will likely be a more dovish Fed.

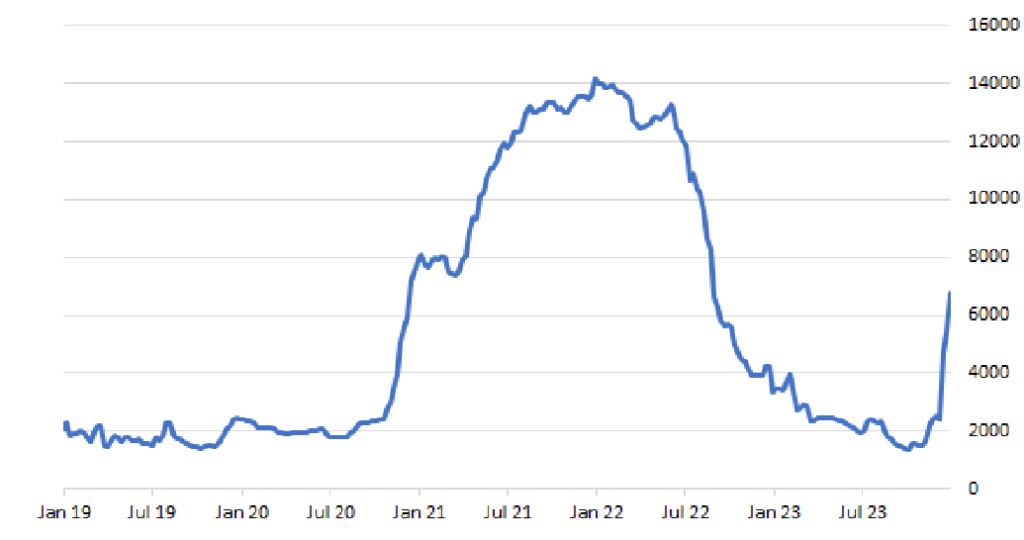

Beyond the rising human cost, geopolitical risk is rising and adding to economic risks. Even if this isn’t evident by looking at markets, it is clear by looking at the transit through the Suez Canal, which has fallen sharply, with ships preferring the longer and more costly route south of the Cape of Good Hope. The chart below illustrates how freight costs went up during lockdown related disruptions and, more recently, how they have spiked due to the conflict in the Middle East, in fact up over four times since November.

Freight costs, China to Mediterranean:

Source: Bloomberg / Freightos Index – 27/01/2019 to 22/01/2024

As mentioned, it’s not just cost, the journeys are taking 20 to 25% longer too. In addition, a serious drought is impacting the Panama canal, which is also a major trade route, albeit less busy than the Suez canal. The impact at a company level is already showing, with companies like Tesla and Volvo suspending some European production.

Despite evidence like higher prices and supply bottlenecks, the market is looking the other way, somehow believing the situation in the Middle East is contained. Instead, the market is focusing on the rate outlook, as it has done for many decades now, stuck on the “more liquidity or less liquidity” playbook.

In our opinion, events in the Middle East add to the inflation outlook, increasingly so if the situation remains unsolved for an extended period. This reinforces our view that rates will remain higher for longer, as inflation reaccelerates.

The Middle East conflict is a fast-moving situation. There are multiple risks, with lots of potential flashpoints. The longer it goes on, the higher the risk of escalation, whether by accident or design. A political solution is needed but looks a long way off.

Anthony Rayner

Premier Miton Macro Thematic Multi Asset Team