In this article, Emma Mogford, Fund Manager of the Premier Miton Monthly Income Fund, provides an outlook for markets over the next 5 years, discussing trends, economies and what this could mean for 2024.

For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Trend is your friend

Often in investing, the ‘trend is your friend’, but from time to time there are significant changes in the backdrop and I believe we are in one of those moments. I think history will look back on 2022 and 2023 as key transition years between the ‘ultra-low’ monetary policy decades and the era of what I call the ‘great rebuild’.

In my opinion the most obvious difference for investors will be that interest rates will remain higher than they have been, although interest rates will look ‘normal’ compared to the decade prior to the global financial crisis, 1998-2008. This will be driven by stickier inflation as we need to spend to replace rather than spend on new. As governments will be involved in the rebuild there will be significant debt issuance which is associated with higher interest rates.

Where to invest?

If I am right and inflation remains sticky, interest rates remain moderate for longer, fiscal policy is expansionary and we see moderate GDP global growth, as we rebuild our infrastructure, I see four key implications for equity investors:

- Protecting clients from inflation. Over the last 100 years equities have proved a useful way of preserving wealth in the face of moderate inflation. If that holds in the next 5 years, then investors will be attracted to companies who can pass through inflation in profits, i.e. strong pricing power, and grow their dividend. It will also favour companies with an installed capacity which will have a competitive advantage over those who need to build new.

- Survival of the fittest. Companies which could previously survive with cheap financing will find life harder. That will make companies with a good return on capital appear more attractive. This is good for our approach of investing in ‘quality’ companies.

- Active stock selection. If company performance becomes more differentiated, according to which companies can finance themselves, deliver returns ahead of their cost of capital and even benefit from acquiring those companies which struggle, then active managers should have a greater edge over passive investing than they did in the last two decades.

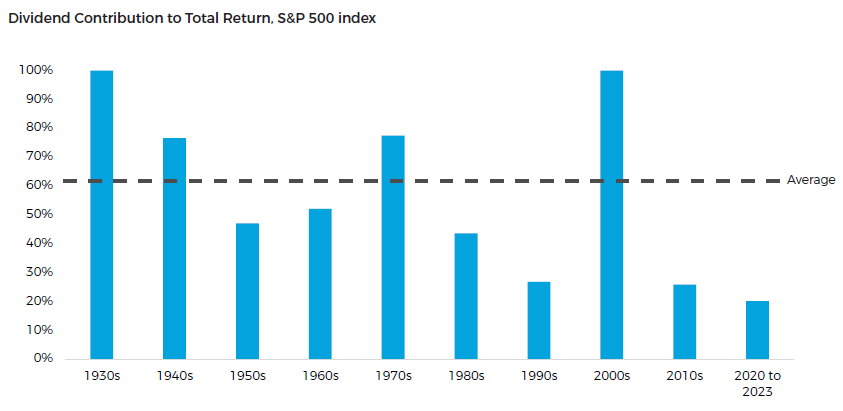

- Importance of dividend. Dividend income used to be a more important portion of an investor’s total return. Without the tailwind of low interest rates, which lifted asset prices, I think they will go back to being important.

Could dividends return to being a more important component of total return in the future?

Source: Bloomberg, data as at 31.03.2023. Past performance is not a reliable indicator of future returns

The great rebuild

I believe 2024 to 2030 will be characterised by what I call the ‘great rebuild’. Much of the ‘rebuild’ will be financed with private capital but public contributions will be meaningful too so governments will need to issue significant amounts of debt, this in turn will keep interest rates above the ultra-low levels seen in the last two decades. With more ‘normal’ interest rates we could return to shorter economic cycles with a recession every 7-8 years. This is healthy for the allocation of capital to the stronger companies. It could lead to a greater divergence in the performance of companies providing plentiful opportunities for active managers.

Both developed and developing economies will be impacted by 3 key trends:

- Rebuild with green. Firstly the need to urgently ‘green’ the economy will require replacing and upgrading energy, industry and transport infrastructure into lower carbon equivalents in the next 20 years. Many of the ‘greener’ options are now cheaper and becoming increasingly so with scale, which will accelerate the pace of change.

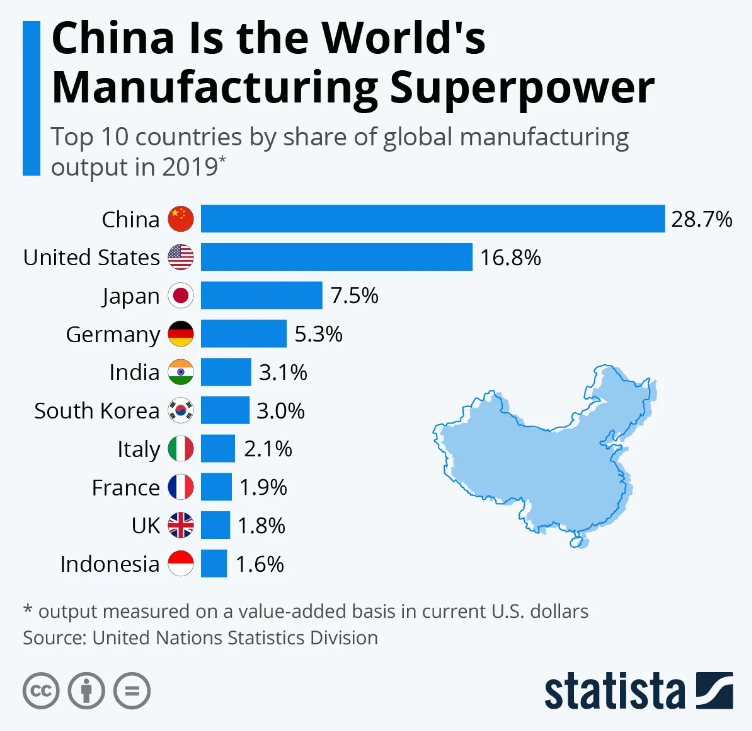

- Rebuild closer to home. The second driving force is the rise of China to superpower status. While the West will continue to rely heavily on China, there will be a significant move to diversify supply chains in order to boost resilience, which will require additional investment in infrastructure in both developed and developing countries.

Source: https://www.statista.com/chart/20858/top-10-countries-by-share-of-global-manufacturing-output/

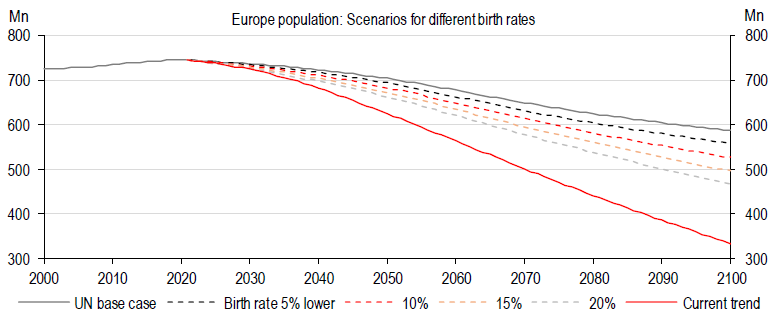

- Rebuild with less people. The final important change is demographics. We will see significant declines in the populations of developed countries in the next couple of decades. For example, the UN predicts a significant fall in the population in Europe, shown below. HSBC are even more pessimistic and see current trend in birth rate as driving the European population to halve by 2050. In particular, the ‘working age’ population will materially fall in some countries. China has particularly challenging demographic headwinds. This will make economic growth harder to come by and could be inflationary given a shortage of workers.

Source: UN Population Division, HSBC estimates. Note: Current trend only goes as low as Korea’s current birth rate, used as a “floor” for any economy.

This will also accelerate the substitution of labour by technology and no doubt automation and robotics as well as AI will play a more meaningful role in 2030. Technology is generally a deflationary force which will help soften other inflationary pressures. There will be investment opportunities within the tech sector, but not ones I am an expert on since they often come with lofty valuations. However, I do see the increasing use of technology with the companies in which we invest, in other sectors, as being underappreciated by the market. I expect it to be a competitive advantage and a key tailwind to profit growth.

Where I could be wrong?

- African GDP growth boom

- Indian contribution to growth will be bigger (I expect India to be an important driver of global GDP growth but expectations here are already high)

- Technology breakthrough

- Geopolitical disaster e.g. China invasion of Taiwan with global repercussions

- Climate disaster (food/immigration/energy)

What it means for 2024?

As we enter 2024, inflation is falling and the market is discounting some sizeable falls in interest rates in the US and UK. For me there are 2 likely scenarios. Firstly, the market’s view of a goldilocks style soft landing where the central banks get the tightening and easing cycle ‘just right’ so as to avoid a recession and avoid higher inflation expectations. This would be positive for equity markets, but I believe a lot is already in the price. I would expect fairly flat global equity market returns but ongoing divergence between countries and sectors.

The second scenario is that the lag in monetary policy, which some commentators put at 18 months, means that we should expect a recession, as monetary conditions continue to tighten. This could be mild or more severe with corresponding negative impact on equity markets. However, I would expect developed market governments to step in with fiscal support as they have done since covid which will limit the extent of equity market falls (although there maybe significant sector divergence). We might experience a significant drawdown in this scenario and I suspect those equities with high valuations where investors have made recent profits (not naming names but the Magnificent 7 look at risk) as well as those businesses in cyclical industries would look most at risk.

Either way 2024 will likely see the market questioning where rates settle. For me that is back at the old ‘normal’ which means we must be wary of valuations that discount rates returning to near 0 levels.

As always, the starting valuation is what matters the most

Over the long-term equities have provided investors with positive returns but this is heavily influenced by the market’s starting valuation. Today I believe the UK offers significant value and hence the prospect for good returns. This is in contrast to the US market (and hence global funds which have significant exposure to the US) where the starting valuation is high relative to history and hence the prospect for returns is lower.

In the scenario of the ‘great rebuild’ UK companies look well placed as there are plentiful opportunities to invest in companies with strong pricing power and already attractive dividends. In particular we remain excited that our philosophy of investing in quality at a reasonable price is particularly well placed.