For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Income strategies fall into two broad camps; pure income focused funds and barbell strategies. We think ours is somewhat different, we call it “third way income”. The pure income strategies focus either on yield (as an identifier of value), or income growth, and tend to do well when income is in favour as a style. The barbell strategies emerged because of the long period when income was out of favour as a style. To address this, managers pursued a growth strategy and bought some very high yield investments to bring the overall yield up. Basically, these are growth funds with some deep value income added in.

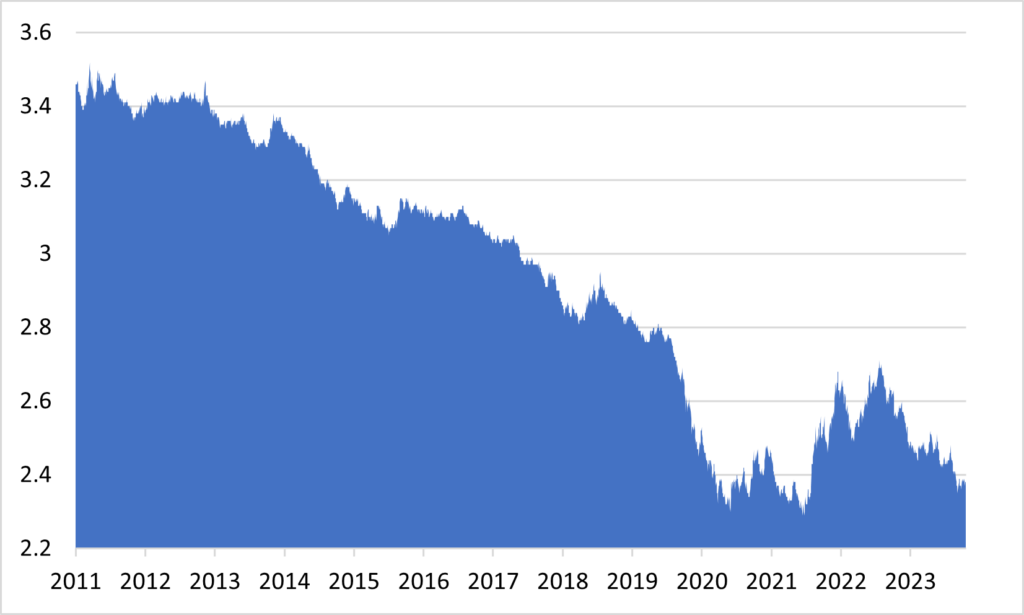

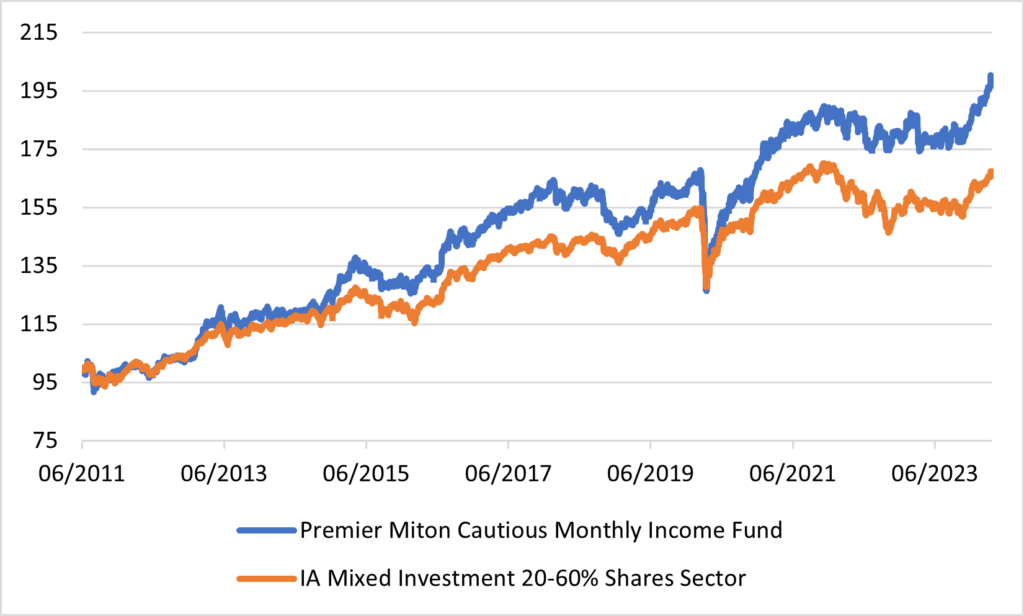

Its not surprising income strategies are not favoured, given the long-term underperformance (see first chart below). We have addressed this with our third way income approach and we are completely pragmatic, in that we are focused on the outcome of the fund, not the inputs. Income growth is the requirement of our income strategies and this needs to grow in line with inflation over time. We think this makes for a very attractive outcome for investors. Importantly, it needs to perform well irrespective of whether any investment style is in favour or not (see second chart).

Long-term underperformance of the FTSE All-World high dividend yield index versus the FTSE World Index (relative)

Source: Bloomberg 09.06.2011 – 26.03.2024

Past performance is not a reliable indicator of future returns.

Premier Miton Cautious Monthly Income Fund vs IA Mixed Investment 20%-60% Shares Sector

Source: FE Analytics. Based on UK Sterling class B Acc, on a total return basis 09.06.2011 – 26.03.2024. Performance is shown net of fees with income reinvested. Rebased to 100.

Past performance is not a reliable indicator of future returns.

We developed our ‘third way income’ strategies out of our main outcome driven multi asset strategies, recognising the growing need for attractive income streams for the rapidly growing pre and post-retirement markets. These original strategies have always had a pragmatic element focusing on risk managed returns over time, with the only consistent feature being the necessity for investments to have positive momentum at entry and the discipline to sell anything with falling momentum.

This discipline meant we could not follow any of the traditional income approaches as they both tend to have periods of strong negative momentum and hence, underperformance. In our view, clients are not satisfied with this lack of consistency.

We apply our existing “evidence, narrative and momentum” disciplines, but with an income feature added. As a result, there are the three key elements of our income strategies. First, pure total return stocks, typically growth stocks, which must meet our momentum criteria and have the role of generating the consistent capital growth that can be reinvested into yielding strategies in equity and bonds to grow the income on the fund.

Next are the rare but precious: strong income growth stocks. Investors, particularly in the US, have a material preference for capital gain over income, so the vast majority of growth stocks now pay no dividends and buy back shares instead. Companies with organic growth that pay a growing dividend are rare these days but are hugely beneficial to our funds. Unfortunately, these are often expensive so our momentum discipline around entry and exit points is important here.

Even more important, is to judge entry and exit points in the pure income stocks. These may be in low growth sectors, or out of favour stocks. They must be out of favour for some reason (a negative narrative) and beginning to show some positive momentum. If we enter at a high yield, collect some dividends, and some good capital return, they can make good investments. However, it is important to remember that these are typically low growth companies and therefore, we must ultimately move on and collect income elsewhere once the yields have fallen. The risk is that you fall into value traps and lose capital value, offsetting the income gain, hence our consistent momentum discipline, negative momentum and they are out.

In the broadest terms, this describes our third way income approach; we look across the whole investment universe, knowing that total returns will always be the key to generating income growth. If we achieve a strong total return, income growth will look after itself and vice versa. This is particularly true with a mixed asset strategy where capital gains can always be reinvested into pure bond income. In rising markets as we see at present, maintaining an appropriate equity weight involves continuous selling. The cash raised can be reinvested to increase the income, this is a daily occurrence in the current markets.

David Jane

Premier Miton Macro Thematic Multi Asset Team