For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

As we have written before, we do not adhere to any dogmatic style of investment management. We are outcome driven investors seeking to offer solutions that meet an intermediary’s client needs. As such, our income funds are not obliged to follow an income style of investing such that you may be familiar with.

An income style of investing involves seeking out either the highest yielding shares or, perhaps, those with the best dividend growth over time. Whilst both are valid approaches, they, like most investment styles, will have periods of poor performance. We think our end investors deserve strong performance across all market conditions.

Hence, we are style agnostic, which may seem a little contradictory given one of our funds is a committed income generating fund. This note will describe income generation in the context of our pragmatic multi asset approach.

We follow a consistently pragmatic approach to investment, we are happy to invest in any region, sector, asset class or style subject to it meeting our investment criteria. These we describe as data, narrative and momentum. Data refers to facts and hard evidence – fundamentals is what most investors call this. Narrative refers to what the market thinks – we look for entry points where the market’s story conflicts with the evidence. Perhaps an area has fallen out of fashion and the reason why it fell out of fashion is no longer the case, but the market hasn’t recognised this. Most importantly though we look for confirmation from momentum in the price, suggesting we are not alone in believing things are improving. You can lose an awful lot of money whilst being right on the fundamentals waiting for the market to agree with you.

We construct our mixed asset portfolios following the macro and thematic ideas we have and using stocks and bonds that meet those criteria above. Many of these investments may be explicitly growth investments, for example, much of our portfolio currently has no yield whatsoever.

This pragmatic approach is best explained with an example.

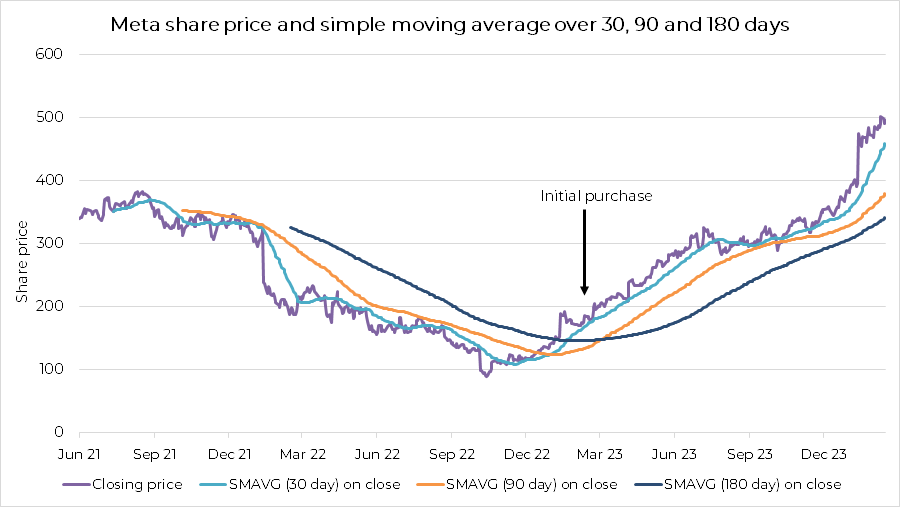

Source: Bloomberg 22.06.21 to 06.03.24. Past performance is not a reliable indicator of future returns.

Following a period of underperformance, Meta, the tech/advertising near monopoly, become very cheap on an earnings basis, in our view, as the market was highly cynical of its Metaverse investments, amongst other things. It had, however, rallied sharply through its moving averages and hence met our momentum criteria also, so we introduced a 1% position (£1.2m at the time). This was bought as part of a basket of stocks in our digital economy theme.

We have a strict position scaling discipline for equities and we typically buy large caps up to 1% and trim before 1.5%. So as a result of the exceptional performance we have been regularly taking profits in the stock, such that sales now amount to nearly two percent of the Premier Miton Cautious Monthly Income fund value.

These profits have been invested in other stocks that also meet our investment criteria, such as Stellantis, the automaker, again meeting our criteria of strong fundamentals but a negative narrative, with strong momentum. In this case also coming with an attractive dividend paid in April. We have several traditional automakers worldwide for similar reasons. This one will generate the Premier Miton Cautious Monthly Income fund £92k of income in April.

As equities rise, we become natural sellers as there is an upper bound to our equity weight. These gains will tend to be reinvested in bonds. A typical corporate bond we have been buying lately for the income would, for the remainder of our Meta sales, generate around another £30k of income over a year.

Our initial 1% investment in Meta now leaves us with a close to 1% position in Meta, a similar position in Stellantis and a corporate bond at about 50bps. And most importantly an income of just over £120k per annum- 10% yield on our initial capital.

This simple example demonstrates our approach to running a pragmatic income fund. We only buy stocks that meet our investment criteria, some of which will be growth stocks. So long as we are carefully managing total return, in both up and down markets, we will always be able to reinvest into attractive stocks with a high yield. There are always high yielding opportunities out there but we never dismiss those stocks with no yield, as to generate a growing income we must have a capital growth over time.

Meta can be an income stock and as the icing on the cake, Meta itself now just started paying a dividend.