Commercial real estate outlook

Alex Ross, manager of the Premier Miton Pan European Property Share Fund, shares why he is ‘Mr. Blue Sky’ when it comes to pan European real estate equities.

For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Material impacts

The last year and a half have been a very painful experience for pan European real estate equities. This has been due to sharply increasing borrowing costs requiring higher property yields – a marked reverse of the ‘easy money’ environment in the decade of ultra-low interest rates.

To account for this new and significantly more expensive financing environment, most areas of our market have already suffered material asset value falls. Amidst the uncertainty on the outlook for interest rates, sentiment has been deeply negative for the under owned and unloved European real estate equities. This fog of negativity has shrouded the sector to the extent that share prices have been trading at a level of discount to asset values only typically seen once in a generation.

Examining the evidence

It is encouraging that we are now starting to see economic evidence that the end of the interest rate tightening cycle is potentially in sight. Historically, after a major downturn like we have witnessed over the last 18 months, property company share prices can rapidly re-rate towards underlying asset values, once equity markets get a sense that underlying property values have reached or are approaching a floor. Thereafter, in the medium term share prices can even move to premiums to these asset values if they believe there could be some asset value recovery ahead.

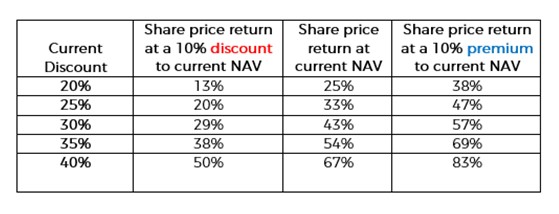

We highlight this as the potential returns from a share re-rating following a steep NAV discount towards the underlying NAV is often underestimated and potential returns can remain significant even after an initial recovery, the theoretical example in the below table demonstrates this:

Source: Premier Miton, for illustrative purposes only.

The key to realising this investment opportunity is to understand the outlook for asset values in our pan European real estate markets. We have already seen a rapid correction in values in the UK, broadly in line with that seen in the early 90’s property downturn, when interest rates reached double digits.

Looking to the east and continental property yields, we have seen these have increased materially, but with a more limited impact on capital values, thanks to most European commercial property leases offering annual inflation-indexation rental uplifts. These have helped offset the negative impact of a higher property yield requirement.

As such, property yields have already significantly adjusted to account for higher borrowing costs. It should be remembered that real estate is not a fixed income asset. Whilst it has offered an easy ‘carry trade’ in the past decade with negligible borrowing costs, traditional property cycles with more normalised higher interest rates have typically required rental growth to deliver attractive returns. This cashflow growth will be key in what we expect will still be an inflationary environment ahead.

We believe more operational property companies that earn the cashflow growth, through regenerating assets or growing cashflows annually with shorter leases in structurally in demand property sub-sectors will flourish into the next property cycle. In contrast, we believe some of the more passive long income ‘asset gathering’ vehicles, which benefitted from the low rates environment, will struggle to deliver key cashflow growth without the tailwind of ultra-low rates.

Inflation at around 3%-4% is where operational property can again demonstrate its inflation-hedging qualities, rather than the runaway inflation that sent real estate markets into cardiac shock with record interest rate rises in this downturn.

View from the property desk

In our view, this cashflow growth potential is the real hidden value in the sector and why it is well positioned for the recovery cycle. Supply in almost all areas of our markets has been limited for several years. This has been due to a combination of restrictive and regulated bank lending on speculative development, increasingly difficult planning in our tight markets; values below replacement costs in certain sub-sectors, economic uncertainty with Covid and Brexit, and increased construction costs.

Against this background of limited supply, we see structural tenant demand, with ‘needs-based’ occupier demand in key areas such as logistics (near shoring), green offices (energy requirements), healthcare (demographics), and purpose-built student accommodation (growth in student number/desire for modern and collaborative accommodation). Even some retail sub-sectors are now seeing rents increasing after the substantial and needed falls in rents and business rates, combined with re-purposing excess un-needed space to alternative uses over recent years.

This combination of elevated property yields combined with tangible rental growth is a rare opportunity in real estate. It has been no surprise to us to see leading private operators firstly stepping into the deeply discounted listed property sector, to acquire companies positioned for this. The latest example of this being our holding in Intervest, which benefitted from a cash bid by TPG last month at a 52% premium to the closing price on the day prior to the shares being suspended. If discounts prevail, we expect more M&A will follow. As a result of this attractive cashflow with income growth potential, we also expect real estate investors to become more active in underlying real estate markets in the coming months. This is of course if data continues to indicate interest rates are close to peaking, and with potential for these peak rates to ease in the medium term.

Looking forward

Importantly, forward looking equity markets will typically reflect this well in advance of the underlying real estate market. This is why we expect share prices to re-rate towards net asset values rapidly when the market gains confidence of these rates peaking.

Furthermore, the rental growth potential inherent across our real estate investments suggest in the medium term we may even see a return to asset value growth in a number of sectors, as yields stabilize or marginally compress and increased annual rents drive capital value growth going forward.

In that scenario, total accounting returns may be at a level that often sees real estate shares trade at premiums in anticipation of this capital growth.

There will doubtless be periods of uncertainty ahead and this thesis is based on a more favourable interest rate direction ahead with excessive inflation brought under control, but the skies appear to be clearing for a potential re-rating opportunity from such discounted levels only witnessed typically once in a generation.