In this latest Market Watch, Neil Birrell, Premier Miton’s Chief Investment Officer, reflects on the interest rates saga and looks at where interest rates could be headed, while sharing why it’s not all bad news.

For information purposes only. Any views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Investing involves risk. The value of an investment can go down as well as up which means that you could get back less than you originally invested when you come to sell your investment. The value of your investment might not keep up with any rise in the cost of living.

Premier Miton is unable to provide investment, tax or financial planning advice. We recommend that you discuss any investment decisions with a financial adviser.

March – in brief

- March came and went with no interest rate cuts to be seen.

- Financial markets look to the future and that is very much the case this year so far.

- The UK is not in that bad a shape it seems.

- Company profits to come back into focus, hopefully.

Not that disappointed, after all

I’m getting a bit bored of writing about interest rates and I would imagine you are getting a bit bored of hearing and reading about them. Hopefully, we are coming towards the end of the saga, but for now, here we go again.

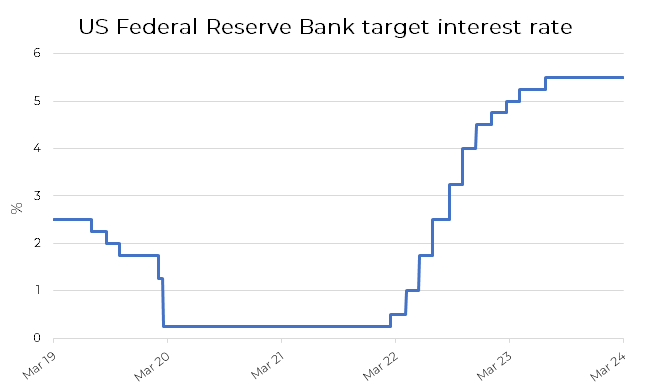

Just before Christmas, financial markets had “priced in” over a 90% chance of the US Federal Reserve cutting their interest rate by 0.25% in March, to be followed by another 5 cuts throughout the year. That means prices at that point in time, in money markets, for example, were taking into account those future expectations. Bond and stock (or equity) markets had moved smartly upwards to reflect those expectations. Even at the time, it felt as though hopes were being stretched too far. The central banks were telling us a different story, that we should not be expecting them to act quickly or decisively; they were being cautious. To act too soon could mean that inflation would reignite as a problem.

As we moved through the first 3 months of 2024, those interest rate cut expectations reversed, back to reflect much more what the central banks were saying. Financial markets did not follow suit though, more of that below.

Source: Bloomberg 30.03.2019 – 31.03.2024. The data points in the chart show the highest figure of the range given by the US Federal reserve for their target interest rate.

The European Central Bank, the Bank of England and the, all important, US Federal Reserve (Fed) all met in March and took no action on interest rates. However, investors did get excited again over the accompanying statements and press conferences, where the tone was more optimistic and we are probably now looking at June or July for the first move. Even though there are arguments over who should move first, it does feel like everyone is waiting for the Fed. In essence, inflation is heading rapidly back towards target levels and economies are remaining quite robust, allowing the turn in the interest rate cycle to be activated.

What goes up, must come down. Really?

As bonds and equities had a very good end to the year, driven by those improving interest rate hopes, you would expect them to reverse as the hopes faded. However, you would be wrong, for the most part.

Bond markets had an amazing final quarter of 2023, but, depending on which part of the bond market you look at, they were either down a small amount or broadly unchanged for the first 3 months of 2024. Meanwhile equities were up strongly in most regions, with the US S&P 500 Index hitting all-time highs near the end of March. Even though the UK lagged behind over the 3 months, it did have a much better March. So, why did equities do so well and bonds do OK?

It’s another case of factors being “priced in” to some extent. In other words, even though the good news didn’t materialise, it was just delayed, and we have been waiting a long time for this. Furthermore, and very importantly, there was good news on inflation and economic growth with the former falling nicely and the latter impressing, with a recession seemingly not a strong possibility. Investors, in aggregate, are willing to look through the short term to the longer term and that was the case in early 2024.

Source: Bloomberg: 31.03.2019 – 31.03.2024

Past performance is not a guide to future returns.

We can be a bit hard on ourselves

It’s quite common for us to knock the UK, whether that be society, politics, the economy or many other facets. I think it’s worth pointing out that there is often a lot of good things to say as well.

In my opinion the economy has remained incredibly resilient though COVID and the stresses posed by high inflation and rising interest rates bringing the “cost of living” crisis into our lives. Even though the government’s budget “for growth” didn’t really feel like that, the economy is doing relatively well. We slipped into the very mildest of recessions in the second half of last year, so mild, in fact, that it barely registered and we are probably out of it already.

The robustness of the economy is largely down to the consumer sector, as evidenced by UK living standards recovering to their highest level in more than 2 years at the end of 2023, as inflation eased, and wage growth jumped. It’s likely this will continue to improve as inflation subsides.

It’s not all good news as economic growth is likely to be sluggish and low relative to other major countries, but it’s not all bad news!

I still haven’t found what I’m looking for, but I might be getting hotter

The prices of bonds, company shares and many other assets from real estate to gold to Bitcoin have, for the most part, been driven by macroeconomic factors, such as inflation, interest rates, economic growth and geo-politics, for some time. This has meant that some parts of the stock markets have done well and some poorly. For example, the giant US technology and communications companies such as Apple, Amazon, Meta (Facebook) and Microsoft have led the way, whilst small companies in the UK have lagged badly, even though their businesses have actually been doing quite well.

There are signs that company fundamentals are now reasserting themselves as drivers of share prices. These are more company specific factors such as growth in revenues, profits and cash generation or management ability or merger and acquisition successes. More recently we have seen a big dispersion in share price returns within those giant US companies, the ones doing well have shown the necessary traits in their fundamentals. Furthermore, small companies in the UK and around the world have sparked into life.

I think there is a good chance this could continue, firstly as interest rates start falling, they become less influential. Secondly, through April we will hear from companies how the first quarter of 2024 has gone, as they announce their trading conditions and profits, as well as commenting on the outlook for the rest of the year. This could well be a catalyst for further focus on company fundamentals.

This would mean that it is vital to be invested in the right companies, not just the right country, industry sector or the stock market overall.

The last word

There’s plenty to be worried about; inflation reviving, interest rates not falling, politics and conflicts. But there is plenty to be optimistic about as well.