Nick Ford, fund manager of the Premier Miton US Smaller Companies Fund, highlights why he believes that history is about to repeat itself with US small caps poised to perform once again.

For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

The AI effect

We had the FANGs in the middle of the last decade, now we have the Magnificent 7. In an investable universe of around 3,000 stocks as represented by the Russell 3000 Index – which includes large, mid and small cap companies – a select few names seem to be endlessly dominating the news headlines. Admittedly, the majority of the “Magnificents” have recently produced outsized share price gains for investors. High performance microchip producer Nvidia has more than tripled in a year and Meta Platforms has more than doubled over the same period. Alphabet, Amazon.com and Microsoft have also had terrific moves while only Tesla has languished.

The common thread driving the best performing Magnificent stocks is Artificial Intelligence. The successful adoption of AI by Microsoft has given it a revolutionary new product cycle because AI significantly enhances its Azure software platform. Both Google and Facebook (owned by Alphabet and Meta Platforms respectively) have been able to improve customer engagement/search capabilities using AI-related algorithms. Amazon has invested vast sums in AI related technologies to strengthen its cloud business and Nvidia’s explosive sales growth has been driven by its AI semiconductors.

The widespread adoption of Artificial Intelligence related tools appears to be accelerating and currently driving the returns of the S&P 500 large cap index because Microsoft, Nvidia, Amazon, Alphabet and Meta Platforms now account for over one fifth of the benchmark. This high level of “concentration” provides both risks and opportunities for investors. If we are witnessing an AI mania and it begins to recede, there are plenty of other US companies with very strong longer term prospects – the “yet-to-be-classified-as-Magnificents” – which might begin to attract more attention.

A history lesson

We have seen similar situations in the past. In the 1970s and 80s, portfolio managers who benchmarked against the S&P 500 Index would have held large positions in the “nifty-fifty” stocks of that time… blue chip companies with records of consistent and steady earnings growth. Magnificent “nifties” might have included Philip Morris, the world’s largest cigarette producer, industrial conglomerate General Electric, pharmaceutical companies Merck and Pfizer, computing giant IBM and Disney.

During the dot com investing era of the late 1990s and early noughties, the most popular and best performing stocks were linked to companies providing access or tools for the internet. Cisco Systems manufactured the critical components to connect corporations to the World Wide Web and America Online provided a dial-up service to millions of Americans. AOL became so big it was able to purchase media conglomerate Time Warner in the largest merger in US history. PC makers Dell and Compaq achieved explosive sales growth as everyone rushed to get online. While these mega caps made headlines across the world, small companies such as Nvidia, Netflix and Amazon.com completed their IPOs, attracting considerably less attention from investors at the time.

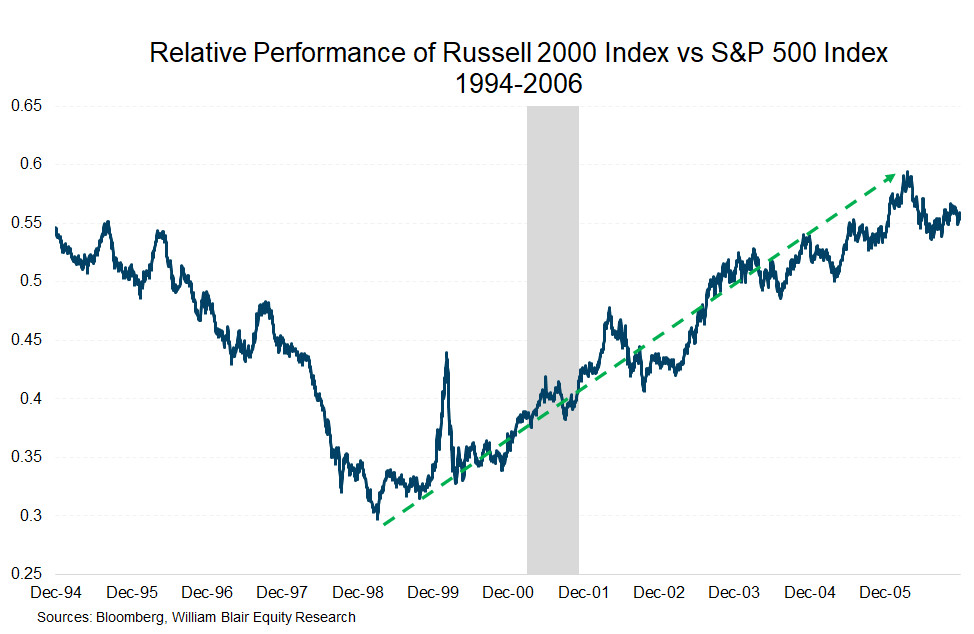

Despite the popularity of the “Magnificents” of this era, investors were actually able to obtain better overall returns from asset classes which had beforehand fallen out of favour. Small and mid-cap stocks in particular began to produce excellent gains and the Russell 2000 Index considerably outperformed the large cap S&P 500 Index benchmark over a seven year period beginning in 1998. In fact, this area of the market was even able to do well ahead of (and throughout) the 2000-2001 economic downturn.

Past performance is not a reliable indicator of future returns.

History repeating itself?

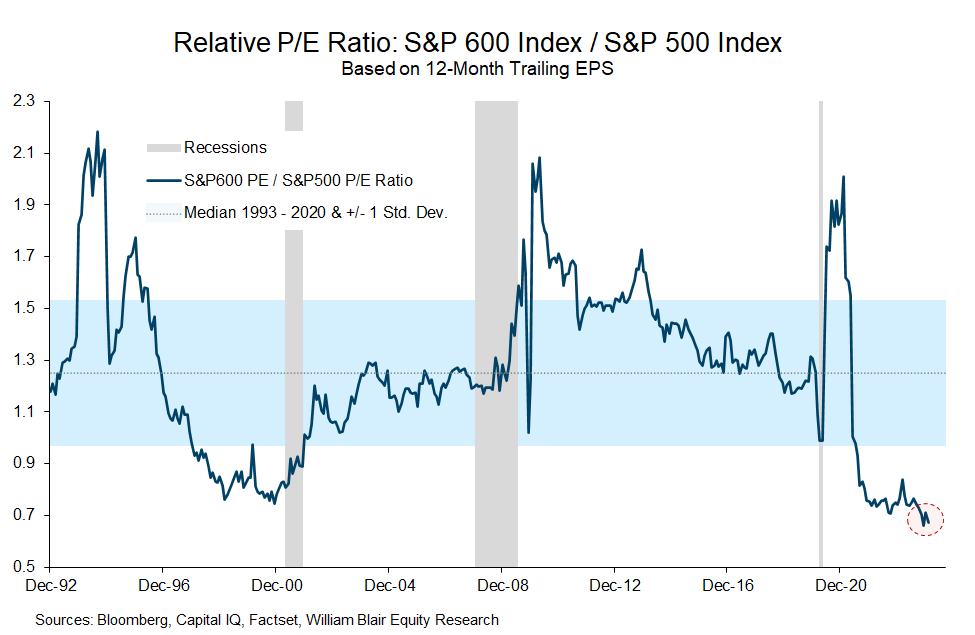

We think the stage may be set for history to repeat itself because valuations of smaller companies now look compelling. Price to earnings multiples stand in stark contrast to not only the Magnificent Seven but also large cap stocks in general. The chart below shows that smaller companies, which normally trade at a 20% premium to large caps (due to their faster growth potential) now trade at a record discount.

Predicting which names within the small cap universe will have the potential to become mega cap giants is challenging but the odds are that we will see some great new companies eventually emerge. Walmart Stores, Salesforce.com, Starbucks, Biogen, Chipotle Mexican Grill and Royal Caribbean Cruises would have been held by small cap portfolio managers in prior decades.

Really successful growth companies (those with unique and valued products or services) are usually first included in the Russell 2000 or S&P 600 Small Cap indices before being upgraded to the S&P 400 Midcap Index and then finally into the S&P 500 Index as they gain market share and increase their revenue base. We prefer to focus on these types of situations – companies which are climbing up the mountain as opposed to those who are already looking down from the summit.